Official Deed in Lieu of Foreclosure Template for Florida

Official Deed in Lieu of Foreclosure Template for Florida

In the state of Florida, homeowners facing financial difficulties may find themselves exploring various options to avoid foreclosure. One significant alternative is the Deed in Lieu of Foreclosure, a legal process that allows a borrower to voluntarily transfer the title of their property back to the lender. This arrangement can be beneficial for both parties, as it typically results in a quicker resolution compared to traditional foreclosure proceedings. By executing this deed, the homeowner relinquishes ownership of the property, while the lender agrees to cancel the mortgage debt, often sparing the borrower from the lengthy and damaging effects of foreclosure on their credit report. The form itself outlines essential details, including the names of the parties involved, a description of the property, and any existing liens. Additionally, it may stipulate terms regarding the condition of the property and any potential liabilities that the borrower may still face. Understanding the implications and requirements of this form is crucial for homeowners considering this route, as it can provide a pathway to financial recovery and a fresh start.

A Deed in Lieu of Foreclosure can be a crucial step in resolving mortgage issues. However, it is often accompanied by several other important documents that help facilitate the process. Below is a list of commonly used forms and documents that you may encounter alongside the Florida Deed in Lieu of Foreclosure.

Understanding these documents is essential for anyone considering a Deed in Lieu of Foreclosure. Each form plays a vital role in ensuring that the process is clear, legal, and beneficial for both parties involved. Be sure to consult with a professional to navigate these documents effectively.

A mortgage modification agreement serves as a tool for homeowners who are struggling to keep up with their mortgage payments. This document allows the lender and borrower to renegotiate the terms of the loan, often resulting in a lower interest rate, extended repayment period, or reduced principal balance. Like a deed in lieu of foreclosure, a mortgage modification aims to prevent foreclosure by making the loan more manageable for the homeowner. Both documents require mutual consent from the lender and borrower, and they seek to find a solution that benefits both parties while avoiding the lengthy and costly foreclosure process.

A short sale agreement is another option for homeowners facing financial difficulties. In a short sale, the homeowner sells the property for less than the amount owed on the mortgage, with the lender's approval. This document is similar to a deed in lieu of foreclosure in that it allows the homeowner to avoid foreclosure and its negative impact on their credit score. Both processes involve the lender's consent, and they serve as alternatives to the traditional foreclosure route. However, a short sale requires finding a buyer for the property, which can add complexity and time to the process.

A forbearance agreement offers a temporary solution for homeowners who can’t make their mortgage payments but expect to regain financial stability soon. In this document, the lender agrees to pause or reduce payments for a specified period. While both forbearance and a deed in lieu of foreclosure aim to assist homeowners in distress, forbearance is a temporary measure, whereas a deed in lieu involves relinquishing the property entirely. Homeowners may choose forbearance if they anticipate a short-term financial setback, while a deed in lieu may be more appropriate for those facing long-term challenges.

Finally, a bankruptcy filing can also provide relief for homeowners struggling with mortgage payments. When a homeowner files for bankruptcy, it can temporarily halt foreclosure proceedings and provide a structured way to manage debts. Like a deed in lieu of foreclosure, bankruptcy offers a path to resolve financial difficulties, but it is a more formal legal process. Bankruptcy may lead to a discharge of certain debts, allowing the homeowner to start fresh. However, it can also have long-lasting effects on credit scores, which is a consideration that homeowners should weigh against the benefits of a deed in lieu.

A Deed in Lieu of Foreclosure is a legal document where a homeowner voluntarily transfers ownership of their property to the lender to avoid foreclosure. This process allows the homeowner to relinquish their mortgage obligations and often helps them avoid the lengthy foreclosure process.

The homeowner signs the Deed in Lieu of Foreclosure, which transfers the property title to the lender. In return, the lender may agree to forgive the remaining mortgage debt. The process typically involves negotiations between the homeowner and the lender to reach a mutual agreement.

One major benefit is that it can help homeowners avoid the negative impacts of foreclosure on their credit score. Additionally, it can provide a quicker resolution than foreclosure proceedings. Homeowners may also have the opportunity to negotiate terms that could include debt forgiveness.

Yes, there can be drawbacks. The homeowner may still face tax implications if the lender forgives a portion of the debt. Additionally, the lender may not accept the Deed in Lieu of Foreclosure if the property has liens or other claims against it. Furthermore, the homeowner may lose any equity they had in the property.

Eligibility often depends on the lender's policies. Generally, homeowners facing financial hardship and who are unable to keep up with mortgage payments may qualify. It’s important for homeowners to communicate openly with their lender about their situation.

First, the homeowner should contact their lender to discuss their financial situation. Next, they should gather necessary documents, such as proof of income and a hardship letter. After that, they can formally request the Deed in Lieu of Foreclosure and negotiate terms with the lender.

Yes, homeowners can still pursue this option even if they are in the foreclosure process. However, it’s crucial to act quickly, as the foreclosure timeline can be strict. Consulting with a legal professional can provide guidance during this time.

Once signed, the lender will typically record the deed with the local government to officially transfer ownership. The homeowner should receive a confirmation of the debt forgiveness, if applicable. The lender will then take possession of the property and may proceed with selling it.

Yes, obtaining legal assistance is often advisable. An attorney can help navigate the complexities of the process, ensure that all paperwork is completed correctly, and protect the homeowner's interests during negotiations with the lender.

A Deed in Lieu of Foreclosure will still impact a homeowner's credit score, but typically less severely than a foreclosure. The exact impact can vary based on individual credit history and the lender's reporting practices. However, it is generally viewed as a better option than going through a full foreclosure.

What Does a Bill of Sale Need to Say - The document serves as a shield against potential misunderstandings between buyer and seller.

Property Deed Form - This form ensures that all parties are on the same page regarding ownership.

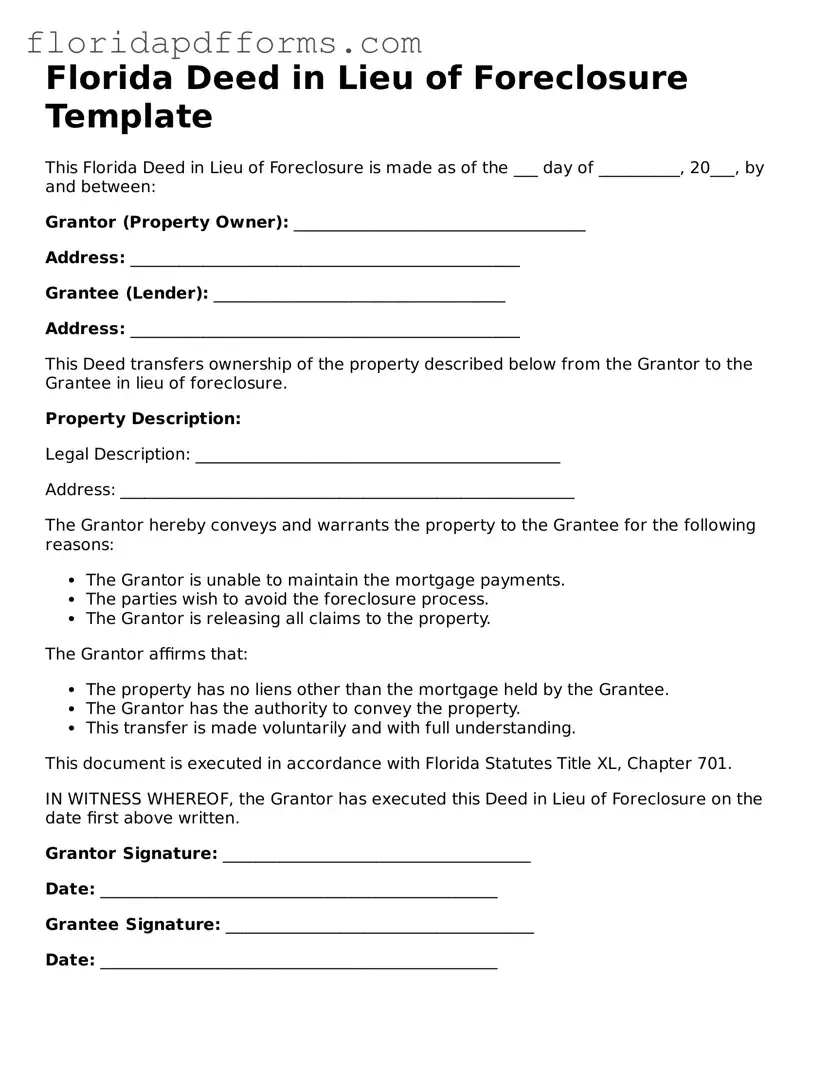

Florida Deed in Lieu of Foreclosure Template

This Florida Deed in Lieu of Foreclosure is made as of the ___ day of __________, 20___, by and between:

Grantor (Property Owner): ____________________________________

Address: ________________________________________________

Grantee (Lender): ____________________________________

Address: ________________________________________________

This Deed transfers ownership of the property described below from the Grantor to the Grantee in lieu of foreclosure.

Property Description:

Legal Description: _____________________________________________

Address: ________________________________________________________

The Grantor hereby conveys and warrants the property to the Grantee for the following reasons:

The Grantor affirms that:

This document is executed in accordance with Florida Statutes Title XL, Chapter 701.

IN WITNESS WHEREOF, the Grantor has executed this Deed in Lieu of Foreclosure on the date first above written.

Grantor Signature: ______________________________________

Date: _________________________________________________

Grantee Signature: ______________________________________

Date: _________________________________________________

When completing the Florida Deed in Lieu of Foreclosure form, it’s important to be careful and informed. Here’s a list of things to do and avoid: