Fill in Your Florida F 1120 Form

Fill in Your Florida F 1120 Form

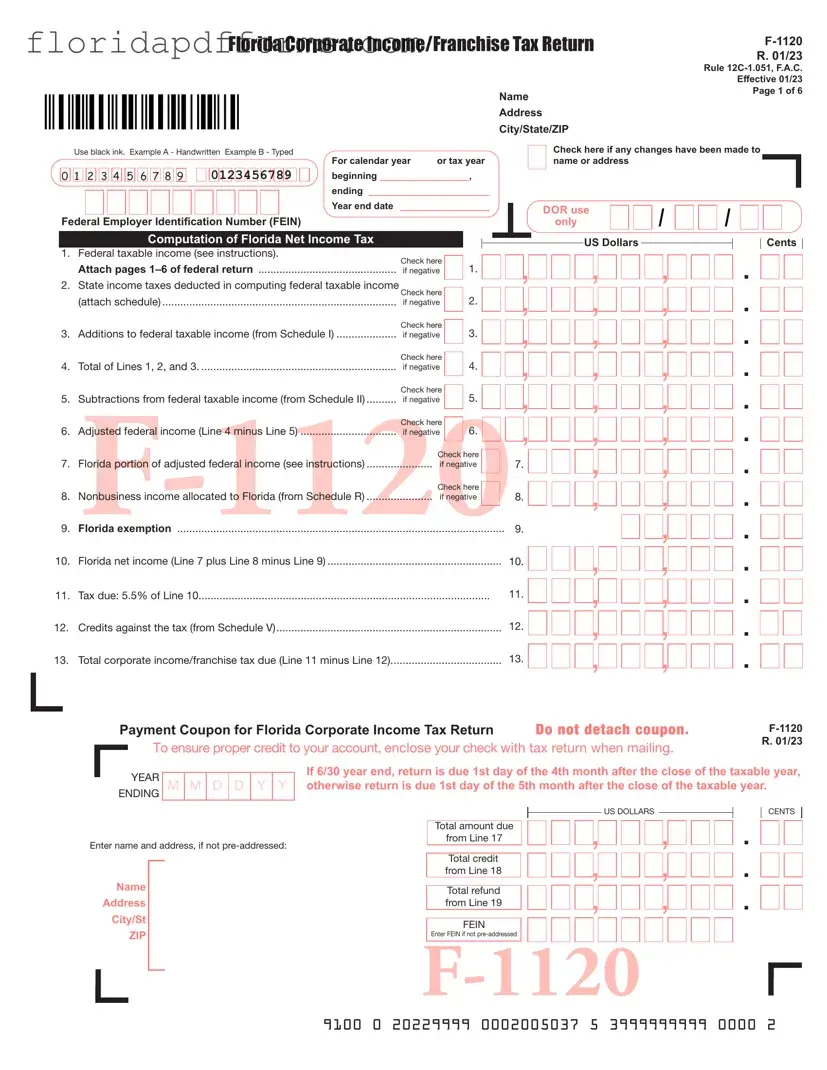

The Florida F 1120 form is a crucial document for corporations operating in the Sunshine State, as it serves as the Corporate Income/Franchise Tax Return. This form is essential for accurately reporting a corporation's income and calculating the corresponding tax obligations. Each year, businesses must disclose their federal taxable income, along with any necessary additions and subtractions, to determine their Florida net income. The form includes specific sections for detailing state income taxes deducted, nonbusiness income allocated to Florida, and various credits that can reduce the overall tax liability. Additionally, it requires the attachment of the federal return and may necessitate supplementary schedules to provide a complete financial picture. Notably, the form also asks for information about the corporation's operations, such as the state of incorporation and whether it is part of a controlled group. Completing the F 1120 accurately is vital; an incomplete return could lead to penalties and delays in processing. With its multifaceted requirements, the F 1120 is not just a tax form but a comprehensive reflection of a corporation's financial activities within Florida.

The Florida F-1120 form is essential for corporations filing their corporate income or franchise tax returns in Florida. Alongside this form, several other documents may be required to ensure a complete and accurate submission. Below is a list of forms that are often used in conjunction with the F-1120.

Each of these forms and schedules plays a crucial role in the tax filing process. Ensuring all necessary documents are submitted will help facilitate a smoother review and processing by the Florida Department of Revenue.

The Florida F-1120 form, which is used for corporate income and franchise tax returns, shares similarities with the federal Form 1120. Both forms require corporations to report their income, deductions, and tax liabilities. They follow a similar structure, asking for information such as gross income, deductions, and tax credits. Just like the F-1120, the federal Form 1120 also requires a declaration under penalties of perjury, emphasizing the importance of accuracy in reporting. The federal form serves as the baseline for corporate taxation, while the Florida form adjusts for state-specific regulations and tax rates.

Another document that resembles the Florida F-1120 is the California Form 100. Like the F-1120, this form is used for corporate income tax reporting at the state level. Both forms require corporations to calculate their net income and apply the appropriate tax rates. They also include sections for reporting various credits and deductions specific to each state. The California Form 100, however, incorporates unique state tax laws and rates, reflecting the differences in corporate taxation between Florida and California.

The New York State Form CT-3 is another document similar to the Florida F-1120. This form is used by corporations operating in New York to report their income and calculate their franchise tax. Both forms require detailed financial information, including income, deductions, and tax credits. They also necessitate the inclusion of a federal return copy as part of the submission. While the CT-3 follows a structure similar to the F-1120, it incorporates New York-specific tax regulations and credits, highlighting the variations in state tax systems.

The Texas Franchise Tax Report is comparable to the Florida F-1120 in that it serves as a state-level tax return for corporations. Both forms require businesses to report their revenue and calculate their tax obligations based on state laws. The Texas report includes sections for deductions and credits, similar to those found in the F-1120. However, the Texas Franchise Tax Report operates under a different tax structure, as Texas does not impose a traditional corporate income tax but rather a franchise tax based on revenue.

The Massachusetts Form 355 is another document that shares similarities with the Florida F-1120. This form is used by corporations in Massachusetts to report their income and calculate their corporate excise tax. Both forms require detailed financial reporting and include sections for various deductions and credits. While the overall purpose is similar, the Massachusetts Form 355 incorporates specific state tax regulations and rates, reflecting the unique tax environment of Massachusetts.

The Illinois Form 1120 is also akin to the Florida F-1120, as both are used for corporate income tax reporting. Each form requires corporations to provide information about their income, deductions, and tax credits. The Illinois form includes specific sections for adjustments to federal taxable income, mirroring the adjustments required in the Florida F-1120. However, the Illinois tax system has its own rules and rates, which differ from those in Florida.

Another similar document is the Pennsylvania Corporate Tax Report (RCT-101). Like the Florida F-1120, this report is used for corporate income tax purposes at the state level. Both forms require corporations to detail their financial activities, including income and deductions. The Pennsylvania form also includes sections for tax credits, similar to those on the F-1120. However, Pennsylvania has its own tax structure and rates, which must be navigated by corporations operating in that state.

The Ohio Commercial Activity Tax (CAT) return is comparable to the Florida F-1120 in that it serves as a state-level tax return for businesses. Both forms require the reporting of revenue, although the CAT focuses on gross receipts rather than net income. Each form includes sections for claiming deductions and credits, but the Ohio CAT operates under a unique tax framework that is distinct from Florida's corporate income tax system.

The Georgia Corporate Income Tax Return (Form 600) also resembles the Florida F-1120. This form is used by corporations in Georgia to report their income and calculate their state tax obligations. Both forms require detailed financial disclosures, including income and deductions. The Georgia form includes sections for tax credits similar to those on the Florida form. However, Georgia's tax rates and regulations differ from those in Florida, necessitating careful compliance with state-specific requirements.

Lastly, the Michigan Corporate Income Tax (CIT) return is another document similar to the Florida F-1120. This return is used by corporations operating in Michigan to report their income and calculate their tax liability. Both forms require a comprehensive breakdown of income and deductions, along with sections for credits. The Michigan CIT operates under a different tax structure, focusing on gross receipts rather than traditional income, which sets it apart from Florida's corporate income tax system.

The Florida F 1120 form is the Corporate Income/Franchise Tax Return that corporations operating in Florida must file. It is used to report income, calculate taxes owed, and claim any applicable credits. This form ensures compliance with Florida tax laws.

Any corporation that is doing business in Florida and is subject to corporate income tax must file the F 1120. This includes both domestic and foreign corporations that have income derived from Florida sources.

The F 1120 is typically due on the first day of the fourth month following the end of the corporation's tax year. For corporations operating on a calendar year, this means the due date is April 1st. If you file for an extension, be sure to check the specific due date for your situation.

To complete the F 1120, you'll need your Federal Employer Identification Number (FEIN), federal taxable income, details about state income taxes deducted, and information regarding any additions or subtractions to federal taxable income. Additionally, you'll need to provide supporting documents, such as a copy of your federal return.

Yes, the F 1120 allows you to claim various credits against your corporate income tax. These may include credits for research and development, enterprise zone jobs, and more. Be sure to attach any required documentation to support your claims.

If you fail to file the F 1120, your corporation may face penalties, including fines and interest on any unpaid taxes. Additionally, not filing can lead to a loss of good standing with the state, which could impact your ability to conduct business in Florida.

Yes, there is a penalty for late filing of the F 1120. The penalty amount can vary, but it typically involves a percentage of the unpaid tax due. To avoid penalties, it’s best to file on time or request an extension if needed.

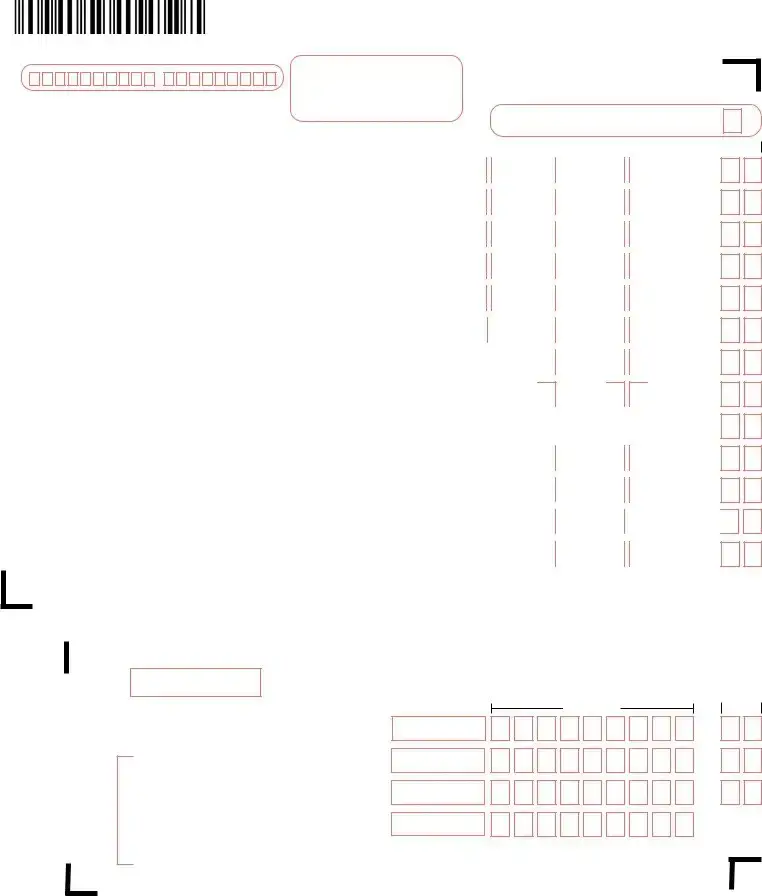

Payments for taxes owed can be made by check, payable to the Florida Department of Revenue. You should mail your payment along with your F 1120 return. If you are requesting a refund, follow the specific mailing instructions provided for that situation.

If you need to amend your F 1120, you should file an amended return. This process typically involves submitting a new F 1120 form marked as amended and including any necessary explanations or documentation to support the changes.

For more detailed information, you can visit the Florida Department of Revenue's website. They provide resources, instructions, and additional guidance to help you navigate the filing process.

Radon Gas Disclosure Florida - It asks for the building's name or ID if applicable.

Florida Bureau of Vital Statistics - If the child’s name has changed, applicants are instructed to indicate the new name.

Florida Corporate Income/Franchise Tax Return |

|

|

R. 01/23 |

|

Rule |

|

Effective 01/23 |

Name |

Page 1 of 6 |

|

|

Address |

|

City/State/ZIP |

|

|

|

Use black ink. Example A - Handwritten Example B - Typed |

For calendar year 2015 or tax year |

|

|

|

|

|

|

|

|

Check here if any changes have been made to |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0123456789 |

|

|

|

|

|

|

|

|

name or address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

0 1 2 3 4 5 6 7 8 9 |

|

|

beginning _________________, 2015 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ending ________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year end date _ _________________ |

|

|

|

|

|

DOR use |

|

|

|

|

|

|

|

/ |

|

|

|

|

|

|

|

|

|

|

|

|

/ |

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

Federal |

|

Employer Identification Number (FEIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

only |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Computation of Florida Net Income Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

US Dollars |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

1. |

Federal taxable income (see instructions). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

||||||||||||||||||||

|

|

Check here |

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

Attach pages |

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

2. |

State income taxes deducted in computing federal taxable income Check here |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

2. |

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

(attach schedule) |

|

|

|

|

|

|

|

|

|

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. |

Additions to federal taxable income (from Schedule I) |

Check here |

|

3. |

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4. |

Total of Lines 1, 2, and 3 |

|

|

|

|

|

|

|

|

|

Check here |

|

4. |

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

, |

|

. |

|

|||||||||||||||||||||||||||||||||||||||||||||||

5. |

Subtractions from federal taxable income (from Schedule II) |

Check here |

5. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

6. |

Adjusted federal income (Line 4 minus Line 5) |

|

Check here |

|

6. |

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

||||||||||||||||||||||

if negative |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7. |

Florida portion of adjusted federal income (see instructions) |

Check here |

|

|

|

|

|

7. |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

8. |

Nonbusiness income allocated to Florida (from Schedule R) |

Check here |

|

|

|

|

|

8. |

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

9. |

|

|

|

exemption |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

10. |

Florida net income (Line 7 plus Line 8 minus Line 9) |

|

|

|

|

|

|

|

10. |

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

11. |

Tax due: 5.5% of Line 10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. |

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

||||

12. |

Credits against the tax (from Schedule V) |

|

|

|

|

|

|

|

12. |

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|||

13. |

Total corporate income/franchise tax due (Line 11 minus Line 12) |

|

|

|

|

|

|

13. |

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

, |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

Cents

Payment Coupon for Florida Corporate Income Tax Return |

Do not detach coupon. |

||

|

To ensure proper credit to your account, enclose your check with tax return when mailing. |

R. 01/23 |

|

|

|||

|

|

||

ENDINGYEAR M  M

M  D

D  D

D  Y

Y  Y

Y

Enter name and address, if not

Name

Address

City/St

ZIP

If 6/30 year end, return is due 1st day of the 4th month after the close of the taxable year, otherwise return is due 1st day of the 5th month after the close of the taxable year.

|

US DOLLARS |

, |

CENTS |

|

Total amount due |

, |

. |

||

|

|

|

||

from Line 17 |

, |

, |

. |

|

Total credit |

||||

|

|

|

||

from Line 18 |

, |

, |

. |

|

Total refund |

||||

|

|

|

||

from Line 19 |

|

|

|

|

FEIN |

|

|

|

|

|

|

|||

Enter EIN if not |

|

|

|

|

9100 0 20229999 0002005037 5 3999999999 0000 2

R.01/23 Page 2 of 6

14. |

a) Penalty: |

b) Other____________________ |

|

||

|

c) Interest: |

d) Other____________________ Line 14 Total u 14. |

|||

15. |

Total of Lines 13 and 14 |

|

|

15. |

|

|

|

|

|

|

|

16. |

Payment credits: Estimated tax payments |

16a |

$ |

|

|

|

|

|

|

|

|

|

Tentative tax payment |

16b |

$ |

16 |

|

|

|

|

|

||

17. |

Total amount due: Subtract Line 16 from Line 15. If positive, enter amount |

|

|||

|

due here. If the amount is negative (overpayment), |

|

|

||

|

enter on Line 18 and/or Line 19 |

|

|

17. |

|

18. |

Credit: Enter amount of overpayment credited to next year’s estimated tax |

|

|||

|

here |

|

|

18. |

|

19. |

Refund: Enter amount of overpayment to be refunded here |

19. |

|||

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

,

.

.

.

.

.

.

.

.

.

.

.

.

This return is considered incomplete unless a copy of the federal return is attached.

If your return is not signed, or improperly signed and verified, it will be subject to a penalty. The statute of limitations will not start until your return

is properly signed and verified. Your return must be completed in its entirety.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Sign here |

|

|

|

Title |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature of officer (must be an original signature) |

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer’s |

|

Preparer |

|

|

Preparer’s |

|||||||||||

Paid |

|

check if self- |

|

|

PTIN |

|

|

|

|

|

|

|

|

|

|

||

signature |

Date |

employed |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

preparers |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

only |

Firm’s name (or yours |

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

if |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and address |

|

ZIP |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

All Taxpayers Must Answer Questions A Through L Below — See Instructions

A.State of incorporation:_______________________________________________________________

B.Florida Secretary of State document number:__________________________________________

C. Florida consolidated return? |

YES q NO q |

D.q Initial return q Final return (final federal return filed)

E.Principal Business Activity Code (as pertains to Florida)

F.A Florida extension of time was timely filed? YES q NO q

Name of corporation: _______________________________________________

H.Location of corporate books:____________________________________________________________

City: __________________________________________ State: ______________ ZIP: ________________

I.Taxpayer is a member of a Florida partnership or joint venture? YES q NO q

J.Enter date of latest IRS audit: ______________

a)List years examined: ____________

K.Contact person concerning this return: _ __________________________________________________

a)Contact person telephone number: (______ )_____________________________________________

b)Contact person email address:_________________________________________________________

L.Type of federal return filed q1120 q1120S or __________________

Where to Send Payments and Returns

Make check payable to and mail with return to: Florida Department of Revenue

5050 W Tennessee Street

Tallahassee FL

If you are requesting a refund (Line 19), send your return to: Florida Department of Revenue

PO Box 6440

Tallahassee FL

Remember:

üMake your check payable to the Florida Department of Revenue.

üWrite your FEIN on your check.

üSign your check and return.

ü

ü

Attach a copy of your federal return.

Attach a copy of your Florida Form

R. 01/23

Page 3 of 6

NAME |

FEIN |

TAXABLE YEAR ENDING |

|

|

|

Schedule I — Additions and/or Adjustments to Federal Taxable Income |

|

|

1. |

Interest excluded from federal taxable income (see instructions) |

1. |

|

|

|

2. |

Undistributed net |

2. |

|

|

|

3. |

Net operating loss deduction (attach schedule) |

3. |

|

|

|

4. |

Net capital loss carryover (attach schedule) |

4. |

|

|

|

5. |

Excess charitable contribution carryover (attach schedule) |

5. |

|

|

|

6. |

Employee benefit plan contribution carryover (attach schedule) |

6. |

|

|

|

7. |

Enterprise zone jobs credit (Florida Form |

7. |

|

|

|

8. |

Ad valorem taxes allowable as an enterprise zone property tax credit (Florida Form |

8. |

|

|

|

9. |

Guaranty association assessment(s) credit |

9. |

|

|

|

10. |

Rural and/or urban |

10. |

|

|

|

11. |

State housing tax credit |

11. |

|

|

|

12. |

Florida tax credit scholarship program credit (credit for contributions to nonprofit |

12. |

|

|

|

13. |

New worlds reading initiative credit |

13. |

|

|

|

14. |

Strong families tax credit (credit for contributions to eligible charitable organizations) |

14. |

|

|

|

15. |

New markets tax credit |

15. |

|

|

|

16. |

Entertainment industry tax credit |

16. |

|

|

|

17. |

Research and development tax credit |

17. |

|

|

|

18. |

Energy economic zone tax credit |

18. |

|

|

|

19. |

s.168(k), IRC, special bonus depreciation |

19. |

|

|

|

20. |

Depreciation of qualified improvement property (see instructions) |

20. |

|

|

|

21. |

Expenses for business meals provided by a restaurant (see instructions) |

21. |

|

|

|

22. |

Film, television, and live theatrical production expenses (see instructions) |

22. |

|

|

|

23. |

Internship tax credit |

23. |

|

|

|

24. |

Other additions (attach schedule) |

24. |

|

|

|

25. |

Total Lines 1 through 24. Enter total on this line and on Page 1, Line 3. |

25. |

|

|

|

Schedule II — Subtractions from Federal Taxable Income

1.Gross foreign source income less attributable expenses

(a) Enter s. 78, IRC, income |

$ _________________________ |

|

(b) plus s. 862, IRC, dividends |

$ _________________________ |

|

(c) plus s. 951A, IRC, income |

$ _________________________ |

1. |

(d) less direct and indirect expenses |

|

Total u |

and related amounts deducted |

|

|

under s. 250, IRC |

$ _________________________ |

|

2.Gross subpart F income less attributable expenses

|

(a) Enter s. 951, IRC, subpart F income $ _______________________ |

2. |

|

|

(b) less direct and indirect expenses $ _______________________ |

Total u |

|

|

|

||

Note: Taxpayers doing business outside Florida enter zero on Lines 3 through 6, and complete Schedule IV. |

3. |

||

3. |

Florida net operating loss carryover deduction (see instructions) |

||

|

|||

|

|

|

|

4. |

Florida net capital loss carryover deduction (see instructions) |

4. |

|

|

|

|

|

5. |

Florida excess charitable contribution carryover (see instructions) |

5. |

|

|

|

|

|

6. |

Florida employee benefit plan contribution carryover (see instructions) |

6. |

|

|

|

|

|

7. |

Nonbusiness income (from Schedule R, Line 3) |

7. |

|

|

|

|

|

8. |

Eligible net income of an international banking facility (see instructions) |

8. |

|

|

|

|

|

9. |

s. 168(k), IRC, special bonus depreciation (see instructions) |

9. |

|

|

|

|

|

10. |

Depreciation of qualified improvement property (see instructions) |

10. |

|

|

|

|

|

11. |

Film, television, and live theatrical production expenses (see instructions) |

11. |

|

|

|

|

|

12. |

Other subtractions (attach schedule) |

12. |

|

|

|

|

|

13. |

Total Lines 1 through 12. Enter total on this line and on Page 1, Line 5. |

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R. 01/23 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 4 of 6 |

||

NAME |

|

|

|

|

|

FEIN |

|

|

|

|

|

|

TAXABLE YEAR ENDING |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Schedule III — Apportionment of Adjusted Federal Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

(b) |

|

|

(c) |

|

|

|

|

(d) |

|

|

|

(e) |

|

|||||

|

|

WITHIN FLORIDA |

|

TOTAL EVERYWHERE |

Col. (a) ÷ Col. (b) |

|

|

|

|

Weight |

|

|

|

Weighted Factors |

|

|||||||

|

|

(Numerator) |

|

(Denominator) |

|

|

Rounded to Six Decimal |

|

If any factor in Column (b) is zero, |

|

Rounded to Six Decimal |

|

||||||||||

|

|

|

|

|

|

|

|

Places |

|

|

see note on Page 9 of the instructions. |

|

Places |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Property (Schedule |

|

|

|

|

|

|

|

|

|

|

|

X 25% or ______ |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Payroll |

|

|

|

|

|

|

|

|

|

|

|

X 25% or ______ |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Sales (Schedule |

|

|

|

|

|

|

|

|

|

|

|

X 50% or ______ |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Apportionment fraction (Sum of Lines 1, 2, and 3, Column [e]). Enter here and on Schedule IV, Line 2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

WITHIN FLORIDA |

|

|

|

|

|

|

TOTAL EVERYWHERE |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

a. Beginning of year |

|

b. End of year |

|

c. Beginning of year |

|

d. End of year |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Inventories of raw material, work in process, finished |

goods |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Buildings and other depreciable assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Land owned |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Other tangible and intangible (financial org. only) assets (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Total (Lines 1 through 4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

Average value of property |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a. Add Line 5, Columns (a) and (b) and divide by 2 (for within Florida)........... 6a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

b. Add Line 5, Columns (c) and (d) and divide by 2 (for total Everywhere) |

|

|

|

|

|

|

|

|

6b. |

|

|

|

|

|

|

|

|||||

7. |

Rented property (8 times net annual rent) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a. Rented property in Florida |

|

|

7a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

b. Rented property Everywhere |

|

|

|

|

|

|

|

|

|

|

7b. |

|

|

|

|

|

|

|

|||

8. |

Total (Lines 6 and 7). Enter on Line 1, Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

a. Enter Lines 6a. plus 7a. and also enter on Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Column (a) for total average property in Florida |

|

|

8a. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

b. Enter Lines 6b. plus 7b. and also enter on Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Column (b) for total average property Everywhere |

|

|

|

|

|

|

|

|

|

|

8b. |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

|

|

(b) |

|

||||||

|

|

|

|

|

|

|

|

|

TOTAL WITHIN FLORIDA |

|

|

TOTAL EVERYWHERE |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

(Numerator) |

|

|

|

(Denominator) |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Sales (gross receipts) |

|

|

|

|

|

|

|

|

|

|

N/A |

|

|

|

|

|

|

||||

2. |

Sales delivered or shipped to Florida purchasers |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

N/A |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Other gross receipts (rents, royalties, interest, etc. when applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

TOTAL SALES (Enter on Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(a) WITHIN FLORIDA |

|

|

(b) TOTAL EVERYWHERE |

|

(c) FLORIDA Fraction ([a] ÷ [b]) |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rounded to Six Decimal Places |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Insurance companies (attach copy of Schedule |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Transportation services |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Schedule IV — Computation of Florida Portion of Adjusted Federal Income |

|

|

|

|

|

|

|

|

|

|

||||||||||||

1. |

Apportionable adjusted federal income from Page 1, Line 6 |

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

2. |

Florida apportionment fraction (Schedule |

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

3. |

Tentative apportioned adjusted federal income (multiply Line 1 by Line 2) |

|

|

|

|

|

|

3. |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

4. |

Net operating loss carryover apportioned to Florida (attach schedule; see instructions) |

|

|

|

|

4. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

5. |

Net capital loss carryover apportioned to Florida (attach schedule; see instructions) |

|

|

|

|

5. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

6. |

Excess charitable contribution carryover apportioned to Florida (attach schedule; see instructions) |

|

|

|

|

6. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

7. |

Employee benefit plan contribution carryover apportioned to Florida (attach schedule; see instructions) |

|

|

|

7. |

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

8. |

Total carryovers apportioned to Florida (add Lines 4 through 7) |

|

|

|

|

|

|

|

|

8. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

9. |

Adjusted federal income apportioned to Florida (Line 3 less Line 8; see instructions) |

|

|

|

|

9. |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R. 01/23

Page 5 of 6

NAME |

|

FEIN |

TAXABLE YEAR ENDING |

|

||||

|

|

|

|

|

|

|||

|

Schedule V — Credits Against the Corporate Income/Franchise Tax |

|

|

|

|

|||

|

1. |

|

Florida health maintenance organization consumer assistance assessment credit (attach assessment notice) |

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

Capital investment tax credit (attach certification letter) |

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

Enterprise zone jobs credit (from Florida Form |

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

|

Community contribution tax credit (attach certification letter) |

|

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

5. |

|

Enterprise zone property tax credit (from Florida Form |

|

|

5. |

|

|

|

|

|

|

|

|

|

|

|

|

6. |

|

Rural job tax credit (attach certification letter) |

|

|

|

6. |

|

|

|

|

|

|

|

|

|

|

|

7. |

|

Urban |

|

|

7. |

|

|

|

|

|

|

|

|

|

|

|

|

8. |

|

Hazardous waste facility tax credit |

|

|

|

8. |

|

|

|

|

|

|

|

|

|

|

|

9. |

|

Florida alternative minimum tax (AMT) credit |

|

|

|

9. |

|

|

|

|

|

|

|

|

|

|

|

10. |

|

Contaminated site rehabilitation tax credit (voluntary cleanup tax credit) (attach tax credit certificate) |

|

|

10. |

|

|

|

|

|

|

|

|

|

|

|

|

11. |

|

State housing tax credit (attach certification letter) |

|

|

|

11. |

|

|

|

|

|

|

|

|

||

|

12. |

|

Florida tax credit scholarship program credit (credit for contributions to nonprofit |

|

12. |

|

||

|

|

|

|

|

|

|

|

|

|

13. |

New worlds reading initiative credit (attach certificate) |

|

|

|

13. |

|

|

|

|

|

|

|

|

|

|

|

|

14. |

|

Strong families tax credit (credit for contributions to eligible charitable organizations) (attach certificate) |

|

|

14. |

|

|

|

|

|

|

|

|

|

|

|

|

15. |

|

New markets tax credit |

|

|

|

15. |

|

|

|

|

|

|

|

|

|

|

|

16. |

|

Entertainment industry tax credit |

|

|

|

16. |

|

|

|

|

|

|

|

|

|

|

|

17. |

|

Research and development tax credit |

|

|

|

17. |

|

|

|

|

|

|

|

|

|

|

|

18. |

|

Energy economic zone tax credit |

|

|

|

18. |

|

|

|

|

|

|

|

|

|

|

|

19. |

|

Internship tax credit |

|

|

|

19. |

|

|

|

|

|

|

|

|

|

|

|

20. |

|

Other credits (attach schedule) |

|

|

|

20. |

|

|

|

|

|

|

|

|

|

|

|

21. |

|

Total credits against the tax (sum of Lines 1 through 20 not to exceed the amount on Page 1, Line 11). |

|

|

21. |

|

|

|

|

|

Enter total credits on Page 1, Line 12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

Schedule R — Nonbusiness Income |

|

|

|

|

|

||

|

Line 1. Nonbusiness income (loss) allocated to Florida |

|

|

|

|

|||

|

|

|

Type |

|

|

Amount |

|

|

_____________________________________ |

|

_____________________________________ |

|

|||||

_____________________________________ |

|

_____________________________________ |

|

|||||

_____________________________________ |

|

_____________________________________ |

|

|||||

|

|

|

Total allocated to Florida |

1. ___________________________________ |

|

|||

|

|

|

(Enter here and on Page 1, Line 8) |

|

|

|

|

|

|

Line 2. Nonbusiness income (loss) allocated elsewhere |

|

|

|

|

|||

|

|

|

Type |

State/country allocated to |

|

Amount |

|

|

_____________________________________ |

____________________________________ |

_____________________________________ |

|

|||||

_____________________________________ |

____________________________________ |

_____________________________________ |

|

|||||

_____________________________________ |

____________________________________ |

_____________________________________ |

|

|||||

|

|

|

Total allocated elsewhere |

2. ___________________________________ |

|

|||

|

Line 3. Total nonbusiness income |

|

|

|

|

|