Fill in Your Florida F 706 Form

Fill in Your Florida F 706 Form

The Florida F 706 form plays a crucial role in the estate tax process, particularly for those dealing with the financial aftermath of a loved one’s passing. This form is essential for both residents and nonresidents of Florida, as it helps determine the estate tax obligations based on the decedent's assets and the applicable federal guidelines. Individuals must complete this form if the estate meets the federal estate tax filing requirements, which can involve a complex interplay of various financial factors. The F 706 form requires detailed information, including the decedent's name, social security number, and residence at the time of death, alongside the names and contact details of the personal representative and any attorneys involved. It also includes sections that specifically address the credits for state death taxes, estate taxes previously paid, and the calculation of any amounts due or overpaid. Understanding the nuances of this form is critical, as it not only affects the financial responsibilities of the estate but also the timely filing and payment of any taxes owed to the state. Moreover, the form must be submitted within nine months of the decedent's death, aligning with federal estate tax requirements. Failure to comply can lead to penalties and interest on unpaid taxes, making it imperative for personal representatives and estate administrators to navigate this process carefully.

The Florida F 706 form is an essential document for reporting estate taxes in Florida. Alongside this form, several other documents are often required to ensure compliance with state and federal regulations. Below is a list of commonly used forms and documents that accompany the Florida F 706 form.

Understanding these accompanying documents is crucial for accurately completing the Florida F 706 form and ensuring compliance with tax obligations. Proper documentation can help streamline the estate settlement process and avoid potential penalties or issues with tax authorities.

The Florida F-706 form, which is the Florida Estate Tax Return, shares similarities with the federal Form 706, also known as the United States Estate (and Generation-Skipping Transfer) Tax Return. Both forms are used to report the value of an estate and calculate any estate taxes owed. The federal Form 706 is required for estates that exceed a certain value threshold, and it includes details about the decedent's assets, debts, and deductions. Similarly, the F-706 form requires information on the estate's value and any taxes already paid to other states, allowing for the calculation of Florida estate tax based on the allowable federal credit for state death taxes. Both forms ultimately serve the same purpose: to ensure compliance with tax obligations following a person's death.

Another document that bears resemblance to the F-706 is the Form 706-NA, which is the federal estate tax return for nonresident aliens. Just like the F-706, the Form 706-NA is used to report estate taxes owed based on the value of assets located within the United States. Both forms require the reporting of gross estate values and any applicable deductions. The F-706, however, specifically focuses on Florida estate tax calculations and includes unique provisions for nonresidents and nonresident aliens, making it essential for those with property in Florida to file the appropriate return.

The Florida Form DR-312, known as the Affidavit of No Florida Estate Tax Due, is another document related to the F-706. This form is utilized when a decedent's estate does not meet the federal estate tax filing requirements, meaning no estate tax is due in Florida. While the F-706 is necessary for estates that exceed certain thresholds, the DR-312 serves as a declaration that no tax is owed, allowing for the removal of any estate tax liens on the property. Both forms are crucial for estate management, but they apply to different circumstances regarding tax obligations.

In addition, the IRS Form 1041, the U.S. Income Tax Return for Estates and Trusts, is similar in that it is used to report income generated by an estate or trust after the decedent's death. While the F-706 focuses on estate taxes, the Form 1041 addresses the income tax responsibilities of the estate. Executors must often file both forms, as they may need to pay estate taxes while also reporting any income earned by the estate's assets. Understanding the interplay between these forms is essential for effective estate administration.

The Florida Form DR-1, the Florida Sales and Use Tax Application, is another document that can be compared to the F-706. While the DR-1 is related to sales tax, it shares the commonality of being a state tax form that requires detailed information regarding the tax obligations of individuals or entities. Both forms require accurate reporting and compliance with state regulations, though they pertain to different types of taxes. The F-706 is focused on estate taxes, while the DR-1 addresses sales tax obligations.

Lastly, the Florida Form F-706-NA, which is a variation of the F-706 for nonresident aliens, is closely related to the F-706. This form is specifically designed for nonresident aliens who have assets in Florida and need to report estate taxes. It mirrors the F-706 in structure and purpose but includes specific provisions and calculations pertinent to nonresident aliens. Both forms are essential for ensuring that estate tax obligations are met according to Florida law, highlighting the importance of accurate reporting for all decedents, regardless of residency status.

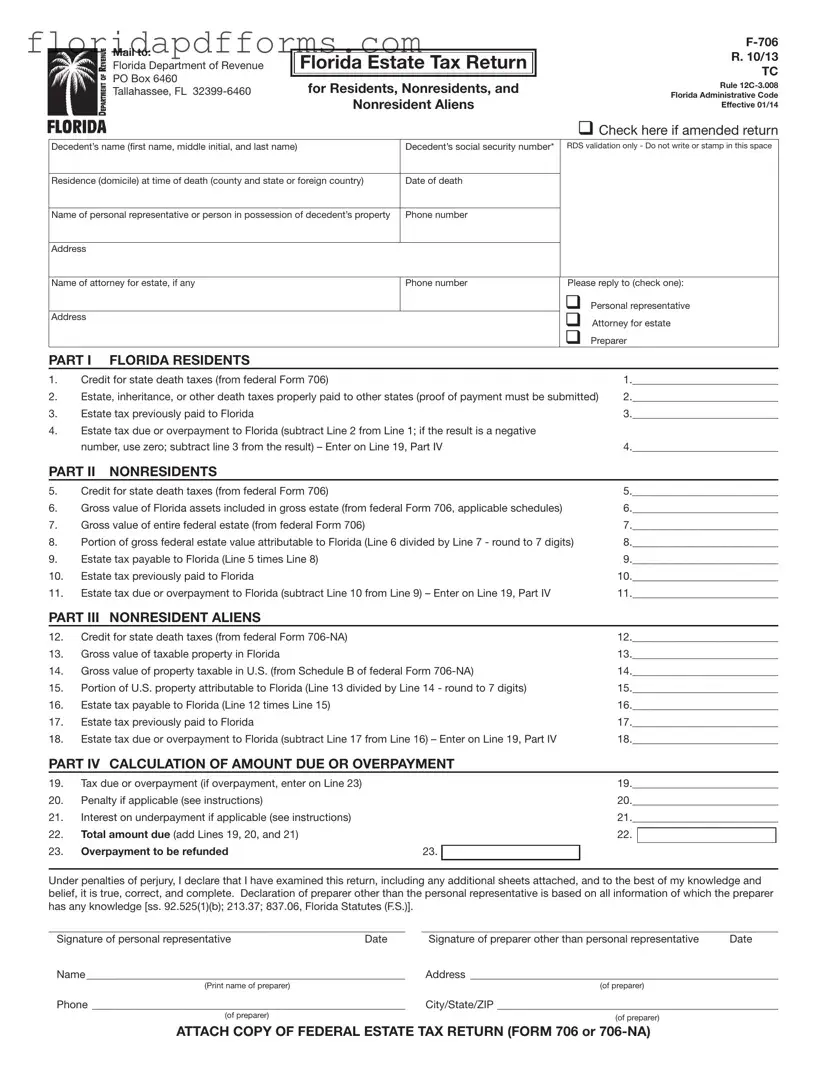

The Florida F 706 form is the Florida Estate Tax Return. It is required for estates that meet certain criteria related to federal estate tax filing requirements. The form helps determine the estate tax due to the state of Florida, based on allowable credits for state death taxes.

The requirement to file the F 706 form depends on the date of the decedent's death. If the death occurred on or before December 31, 2004, a form must be filed for every Florida resident, nonresident, and nonresident alien with Florida property, provided they are required to file a federal estate tax return (Form 706 or Form 706-NA). For deaths on or after January 1, 2005, the form is no longer required.

The F 706 form and any associated payment are due within nine months after the decedent’s death, coinciding with the due date for the federal estate tax return. If you need more time to file or pay, you must request an extension from the IRS, as Florida does not have a separate extension form.

If the tax is not paid by the due date, a late payment penalty will apply. Initially, this penalty is 10% of the unpaid tax. After 30 days, it increases to 20%. Additional penalties may apply if the unpaid tax is due to negligence or intentional disregard of tax laws.

If you need to amend a return, complete a new F 706 form and check the box indicating it is an amended return. If the amendment is due to changes in the federal Form 706 or 706-NA, include a statement explaining the changes and any relevant documents, such as correspondence from the IRS.

Mail your completed F 706 form and payment to the Florida Department of Revenue at the following address:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL 32399-6460

Florida Ethics - The requirements outlined in the form aim to streamline the transfer process between institutions.

Application for Home Health Agency - Applications will be thoroughly reviewed for compliance with the established regulations.

Mail to:

Florida Department of Revenue

PO Box 6460

Tallahassee, FL

|

||

Florida Estate Tax Return |

R. 10/13 |

|

TC |

||

|

||

for Residents, Nonresidents, and |

Rule |

|

Florida Administrative Code |

||

|

||

Nonresident Aliens |

Effective 01/14 |

q Check here if amended return

Decedent’s name (first name, middle initial, and last name) |

Decedent’s social security number* |

RDS validation only - Do not write or stamp in this space |

|

|

|

Residence (domicile) at time of death (county and state or foreign country) |

Date of death |

|

|

|

|

Name of personal representative or person in possession of decedent’s property |

Phone number |

|

|

|

|

Address |

|

|

|

|

|

Name of attorney for estate, if any |

Phone number |

Please reply to (check one): |

|

|

q Personal representative |

Address |

|

q Attorney for estate |

|

|

|

|

|

q Preparer |

PART I FLORIDA RESIDENTS

1. |

Credit for state death taxes (from federal Form 706) |

1.___________________________ |

2. |

Estate, inheritance, or other death taxes properly paid to other states (proof of payment must be submitted) |

2.___________________________ |

3. |

Estate tax previously paid to Florida |

3.___________________________ |

4.Estate tax due or overpayment to Florida (subtract Line 2 from Line 1; if the result is a negative

|

number, use zero; subtract line 3 from the result) – Enter on Line 19, Part IV |

4.___________________________ |

|||||

PART II |

NONRESIDENTS |

|

|

|

|

|

|

5. |

Credit for state death taxes (from federal Form 706) |

|

|

5.___________________________ |

|||

6. |

Gross value of Florida assets included in gross estate (from federal Form 706, applicable schedules) |

6.___________________________ |

|||||

7. |

Gross value of entire federal estate (from federal Form 706) |

|

|

7.___________________________ |

|||

8. |

Portion of gross federal estate value attributable to Florida (Line 6 divided by Line 7 - round to 7 digits) |

8.___________________________ |

|||||

9. |

Estate tax payable to Florida (Line 5 times Line 8) |

|

|

9.___________________________ |

|||

10. |

Estate tax previously paid to Florida |

|

|

10.___________________________ |

|||

11. |

Estate tax due or overpayment to Florida (subtract Line 10 from Line 9) – Enter on Line 19, Part IV |

11.___________________________ |

|||||

PART III |

NONRESIDENT ALIENS |

|

|

|

|

|

|

12. |

Credit for state death taxes (from federal Form |

|

|

12.___________________________ |

|||

13. |

Gross value of taxable property in Florida |

|

|

13.___________________________ |

|||

14. |

Gross value of property taxable in U.S. (from Schedule B of federal Form |

14.___________________________ |

|||||

15. |

Portion of U.S. property attributable to Florida (Line 13 divided by Line 14 - round to 7 digits) |

15.___________________________ |

|||||

16. |

Estate tax payable to Florida (Line 12 times Line 15) |

|

|

16.___________________________ |

|||

17. |

Estate tax previously paid to Florida |

|

|

17.___________________________ |

|||

18. |

Estate tax due or overpayment to Florida (subtract Line 17 from Line 16) – Enter on Line 19, Part IV |

18.___________________________ |

|||||

PART IV CALCULATION OF AMOUNT DUE OR OVERPAYMENT |

|

|

|

||||

19. |

Tax due or overpayment (if overpayment, enter on Line 23) |

|

|

19.___________________________ |

|||

20. |

Penalty if applicable (see instructions) |

|

|

20.___________________________ |

|||

21. |

Interest on underpayment if applicable (see instructions) |

|

|

21.___________________________ |

|||

22. |

Total amount due (add Lines 19, 20, and 21) |

|

|

22. |

|

|

|

|

|

|

|

||||

23. |

Overpayment to be refunded |

23. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any additional sheets attached, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer other than the personal representative is based on all information of which the preparer has any knowledge [ss. 92.525(1)(b); 213.37; 837.06, Florida Statutes (F.S.)].

__________________________________________________________________ |

__________________________________________________________________ |

||

Signature of personal representative |

Date |

Signature of preparer other than personal representative |

Date |

Name___________________________________________________________ |

Address _________________________________________________________ |

||

(Print name of preparer) |

|

(of preparer) |

|

Phone __________________________________________________________ |

City/State/ZIP ____________________________________________________ |

||

(of preparer) |

|

(of preparer) |

|

|

|

|

|

ATTACH COPY OF FEDERAL ESTATE TAX RETURN (FORM 706 or

INSTRUCTIONS FOR FORM

R.10/13 Page 2

General Information

Florida’s estate tax is based on the allowable federal credit for state death taxes. Florida tax is imposed only on those estates subject to federal estate tax filing requirements and entitled to a credit for state death taxes (Chapter 198, F.S.). Estate tax is not due if a federal estate tax return (Form 706 or

Form

The requirement to file Form

Date of Death |

|

|

|

On or before December 31, 2004 |

Yes** |

|

|

On or after January 1, 2005 |

No |

|

|

**If required, Form

Due Dates and Extensions of Time

Form

us within 30 days of mailing the request and 30 days of receiving the federal approval. An extension of time to file does not extend the time to pay. Interest accrues on the Florida tax due from the original due date until paid.

Tax Paid to Other States

For Florida residents: if estate, inheritance, or other death taxes were properly paid to other states, proof of payment must be submitted to the Florida Department of Revenue. (Proof of payment means the final certificate of payment showing the specific amounts of tax, penalty, or interest assessed and paid.)

*Social Security Numbers

Social security numbers (SSNs) are used by the Florida Department of Revenue as unique identifiers for the administration of Florida’s taxes. SSNs obtained for tax administration purposes are confidential under sections 213.053 and 119.071, Florida Statutes, and not subject to disclosure as public records. Collection of your SSN is authorized under state and federal law. Visit our Internet

site at floridarevenue.com and select “Privacy Notice” for more information regarding the state and federal law governing the collection, use, or release of SSNs, including authorized exceptions.

Where to File

Mail your completed

Tallahassee, FL

If you are requesting a nontaxable certificate, include the $5.00 fee.

Signature

The personal representative must sign the return declaration under penalties of perjury. If someone else prepares the return, the preparer must also sign the return.

Amending Form

If you must change a return that has already been filed, you must complete another Form

Penalties and Interest

Penalties – If tax is not paid by the due date (or approved extension date) a late payment penalty of 10% of the unpaid tax is due. After 30 days, the late penalty increases to 20%. An added penalty of 10% per month up to a maximum of 50% of the tax due is imposed if the unpaid tax is due to negligence or intentional disregard. A fraud penalty of 100% of the tax due is imposed if the unpaid tax is due to willful intent to defraud. However, the Department of Revenue is authorized to compromise or settle these penalties pursuant to section 213.21, F.S.

Interest – Interest is due on late payments from the due date until paid. Interest rates are updated January 1 and July 1 of each year. To obtain current interest rates, visit our website at floridarevenue.com.

Need Assistance?

Information and forms are available on our Internet site at

floridarevenue.com.

If you have any questions, you may contact Taxpayer Services at

For a written reply to your tax questions, write:

Taxpayer Services MS

Florida Department of Revenue

5050 W Tennessee St

Tallahassee, FL

For federal estate tax information or forms, visit the IRS website at www.irs.gov.

When filling out the Florida F 706 form, here are ten important dos and don'ts to keep in mind: