Official Loan Agreement Template for Florida

Official Loan Agreement Template for Florida

The Florida Loan Agreement form serves as a crucial document in the realm of lending, outlining the terms and conditions under which a borrower receives funds from a lender. This form typically includes essential details such as the loan amount, interest rate, repayment schedule, and any collateral that may secure the loan. Additionally, it delineates the rights and responsibilities of both parties, ensuring clarity and mutual understanding. Provisions regarding late fees, default consequences, and dispute resolution mechanisms are often included to protect the interests of both the lender and borrower. By establishing a clear framework for the loan transaction, the Florida Loan Agreement form aims to foster transparency and trust between the involved parties, ultimately contributing to a smoother lending process. Understanding the nuances of this form is vital for both borrowers seeking financial assistance and lenders aiming to safeguard their investments.

When entering into a loan agreement in Florida, several other forms and documents may be necessary to ensure that both parties are protected and that all legal requirements are met. Understanding these additional documents can help you navigate the lending process more smoothly.

Being aware of these documents can significantly enhance your understanding of the loan process and help ensure that all parties are aligned and protected. Always consider consulting with a legal professional to guide you through these important steps.

The Florida Loan Agreement form shares similarities with a Promissory Note. Both documents outline the terms under which a borrower agrees to repay a lender. A Promissory Note typically focuses on the borrower's promise to pay back a specific amount of money, often including details like interest rates and repayment schedules. While the Loan Agreement may encompass broader terms, including collateral and obligations of both parties, the Promissory Note serves as a more straightforward acknowledgment of debt. Together, they create a comprehensive understanding of the borrowing arrangement.

Another document that resembles the Florida Loan Agreement is the Security Agreement. This document is crucial when a loan is secured by collateral. Like the Loan Agreement, it specifies the terms of the loan but goes further by detailing the assets pledged as security for the repayment. In essence, while the Loan Agreement outlines the loan's general terms, the Security Agreement provides the necessary legal framework to protect the lender's interests in the event of default. Both documents work together to create a clear picture of the financial arrangement and the associated risks.

A third document that parallels the Florida Loan Agreement is the Mortgage Agreement. This is particularly relevant in real estate transactions where a property is used as collateral for a loan. The Mortgage Agreement details the borrower's obligation to repay the loan while granting the lender a lien on the property. Similar to the Loan Agreement, it includes terms such as the loan amount, interest rate, and repayment schedule. However, the Mortgage Agreement is specifically tailored for real estate transactions, emphasizing the lender's rights regarding the property, should the borrower fail to meet their obligations.

Lastly, the Florida Loan Agreement is akin to a Lease Agreement in certain contexts, especially when financing personal property or equipment. Both documents establish a contractual relationship between a lender and a borrower or lessee. A Lease Agreement outlines the terms under which one party rents property from another, including payment terms and duration. Although the primary focus of a Lease Agreement is on the use of the property rather than ownership, both agreements require clear terms to protect the interests of both parties and ensure that obligations are met. This shared purpose highlights the importance of well-defined agreements in various financial transactions.

A Florida Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a lender and a borrower. This agreement specifies the amount borrowed, the interest rate, repayment schedule, and any collateral involved. It serves to protect both parties by clearly defining their rights and responsibilities.

Anyone who is lending or borrowing money in Florida should consider using a Loan Agreement form. This includes individuals, businesses, and financial institutions. By having a formal agreement, both the lender and borrower can avoid misunderstandings and have a clear reference point in case of disputes.

A comprehensive Florida Loan Agreement typically includes the following key components:

Yes, a Florida Loan Agreement can be modified, but both parties must agree to the changes. It is advisable to document any modifications in writing to avoid confusion in the future. This ensures that both the lender and borrower are on the same page regarding the new terms.

If a borrower defaults on a loan, the lender has several options. They may pursue legal action to recover the owed amount, especially if collateral was involved. The specifics of the default process should be outlined in the Loan Agreement, detailing the steps the lender can take to protect their interests.

How to Prove Residency in Florida - This documentation reinforces your status as a resident in legal contexts.

Florida Vehicle Gift Form - Using this affidavit, one can clarify inaccuracies caused by clerical errors.

Florida Independent Contractor Agreement - It provides a framework for resolving disputes that may arise during the contract term.

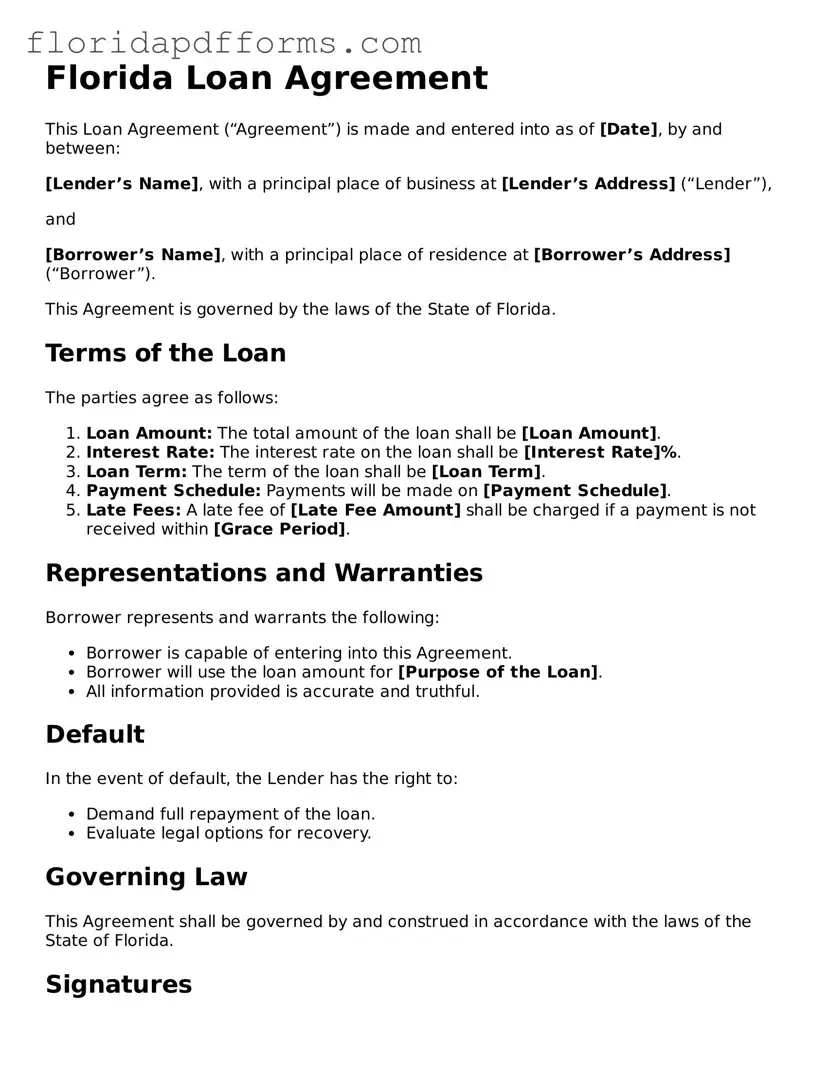

Florida Loan Agreement

This Loan Agreement (“Agreement”) is made and entered into as of [Date], by and between:

[Lender’s Name], with a principal place of business at [Lender’s Address] (“Lender”),

and

[Borrower’s Name], with a principal place of residence at [Borrower’s Address] (“Borrower”).

This Agreement is governed by the laws of the State of Florida.

Terms of the Loan

The parties agree as follows:

Representations and Warranties

Borrower represents and warrants the following:

Default

In the event of default, the Lender has the right to:

Governing Law

This Agreement shall be governed by and construed in accordance with the laws of the State of Florida.

Signatures

By signing below, both parties confirm that they agree to the terms of this Loan Agreement.

Lender Signature: _______________________________ Date: ________________

Borrower Signature: _____________________________ Date: ________________

When filling out the Florida Loan Agreement form, it's important to be thorough and careful. Here are some key dos and don'ts to keep in mind: